Credit Card Catch - Chase PerfectCard

I have a Chase PerfectCard and one thing I like about it is that it has a straight 1% cash rebate and it's immediately credited to your next billing statement. There's no need to wait until you accumulate up to $100 rebate.

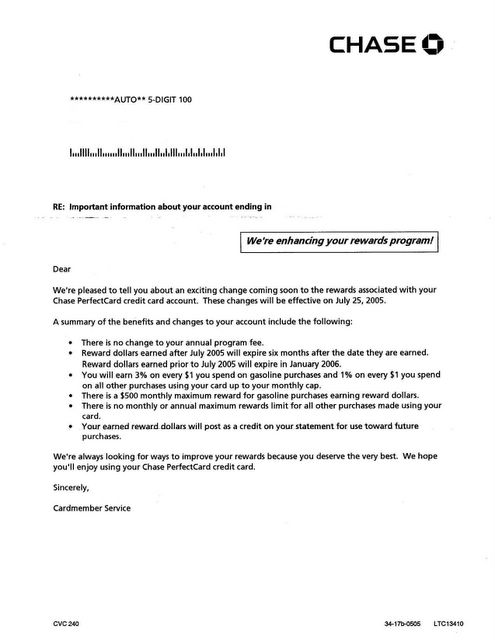

This card sounds too good to be true. I wonder what the "catch" is. Then when I read this letter (see image below) they just sent to me and I realize their business strategy. I feel like I crack the code. There's a part on the letter that states, "Reward dollars... will expire six months after the date they are earned." Unlike other cash rebate cards that write you checks, the Chase Perfect card rebates must be applied as a credit to your future billing statement. Their master plan is to keep you using the card. You need a outstanding balance to take advantage of the rebates. Of course, the more you use it, the more business Chase gets. Ingenious business strategy! What a smart/slick way to keep cardholders charging the cards. And many people use the card for recurring bill payments anyway, so they will not be affected by the "catch."

Chase Letter

Here are the other credit cards, I currently have:

AT&T Universal Card - Great card. Used frequently.

Chase Letter

Here are the other credit cards, I currently have:

AT&T Universal Card - Great card. Used frequently.

- Straight 1% thereafter. Can claim check once rebate accumulates to $50. Best part: 5% rebate intro period for 6-months.

- 1 point per dollar. Best part: Points do NOT expire.

- Rebates based on a tier system, have to work your way up to 1% rebate. Best part: Double rebate value with gift certificates.

- 1% on non-Amazon.com purchases. Best part: 3% rebate on Amazon.com purchases.

posted by Sean @ 5/19/2005 10:00:00 AM

![]()

![]()

4 Comments:

Smarty... I'd blank out that "barcode-ish" part of the letter too, someone with too much time on their hands can derive your ZIP+4 from it.

http://www.smsu.edu/postal/P-glossary.htm#4

Of course, it might not matter to you because everyone knows you live in NY, NY. :)

Thanks for the info, but I think the zip is okay. NYC is a very crowded area. There are thousands and thosands of people in one zip code. I'd be more concern if the barcode gives out the address.

actually I got a smiliar letter too for my Chase Ultimate Rewards Card.

they're switching it to the "Flexible Rewards" program. (the program Bank One had)

seems like they're doing it across the board, "enhancing" many programs. yay us.

another popular cash rebate card is the Citi Dividend, 1% back on all purchases with 5% on everyday purchases (gas, groceries, etc)

there's a cap of max $300 in cash back (or was it $600?) annual, but still good.

same sort of term popped up too, ur reward points will now expire in 6 months. before it never expired, and I believe some certain rebates cost less.

never used the card anyway, I just got it for a balance transfer offer.

All "reward credit cards" have some type of catch. You just have to read the fine print and make sure you follow all the rules. Of course, the credit card company wants you to skip over the fine print so they can make money! Make sure you understand the limitations and benefits of your card so you can make the most out of your rewards card!

Post a Comment

<< Home